Value Investing: Why the P/E Ratio Tells You Almost Nothing

Earnings are an accounting construct. Cash is not. Here is the number professionals use instead — and the hurdle it has to clear before a stock is worth owning.

Value Investing: Why Billionaires Ignore the P/E Ratio

Prefer to watch? This article is the written companion to the video above.

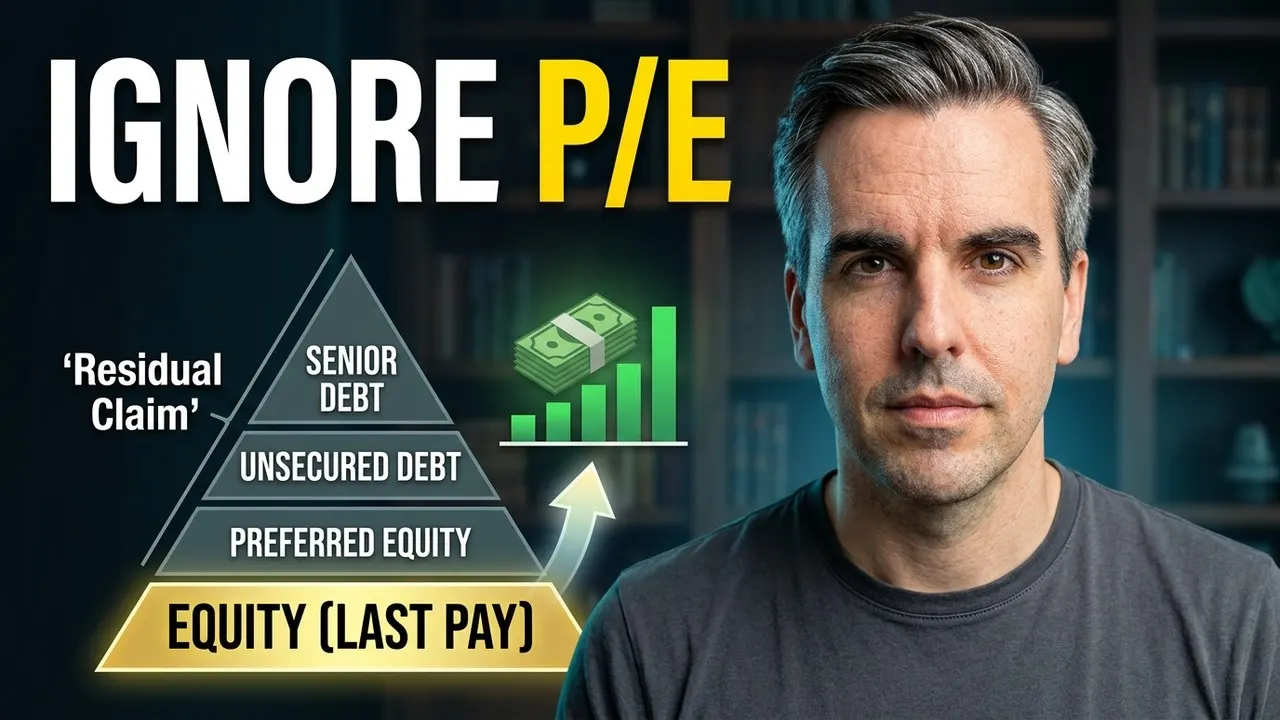

Stop for a second and read what you actually own.

If the company whose shares you hold goes bankrupt tomorrow, here is the order in which the money goes out:

- The tax authority

- Secured creditors — the banks

- Bondholders

- Suppliers

- Employees

- You

You are last. After the banks. After the bondholders. After the person who cleans the office.

That is not a footnote in the prospectus. That is the definition of equity. You own the residual claim — whatever is left over once everybody with an actual contract has been paid, which in a real bankruptcy is frequently nothing at all.

It is also the single most important fact about the asset, and almost nobody who buys shares has consciously registered it.

So why on earth would you accept that?

Because of what sits on the other side of the trade.

A bondholder has priority. They get paid first. And their upside is capped — if the company invents something that changes the world, the bondholder still collects their fixed coupon and not one cent more.

A shareholder gives up the priority and receives, in exchange, everything that is left after the bills are paid. With no ceiling.

You have traded safety for unlimited upside. That is a perfectly rational trade.

But it means the only sane way to value your position is to ask: how much cash can this thing actually hand me?

Which is where most retail analysis goes wrong on the very first step.

The P/E ratio is measuring the wrong thing

The price-to-earnings ratio is the gold standard of retail investing, and to a professional it is often close to useless.

The problem is the E.

Earnings are an accounting construct. They are shaped by depreciation policy, by non-cash charges, by one-off adjustments, by when a cost is recognised versus when it is paid.

None of that is necessarily dishonest. It is simply what accounting is.

But it means the denominator of the most-quoted ratio in the market is a number over which management has genuine discretion.

Cash is much harder to fake.

(In one asset class the distortion is total: a REIT’s earnings are systematically understated by depreciation on buildings that are not actually losing value. The P/E on a REIT is not conservative — it is wrong.)

The number professionals use instead

Free cash flow yield.

FCF Yield = Free Cash Flow ÷ Market CapitalisationFree cash flow is what is left after the company has paid for everything required to keep operating and investing. It is the money that could genuinely reach you — as a dividend, or as a buyback.

A €10bn company generating €500m of free cash flow has a 5% FCF yield.

That is the closest thing equity analysis has to a hard number, and it is the one to anchor on.

Where the warning zones are

Below ~2% — you are paying an enormous premium for growth that has not happened yet. The entire thesis rests on the future being generous. That can work. It is not investing so much as underwriting a forecast.

Above ~8% — be suspicious rather than delighted. A very high yield often means the market believes the cash flow is not going to persist. Cheap is not the same as underpriced, and a business in structural decline can look like a bargain right up until it isn’t.

Roughly 4–8% — a business generating real cash, priced as neither a miracle nor a corpse.

And now the hurdle it has to clear

A free cash flow yield in isolation means nothing. The question is always: compared to what?

The alternative is a government bond that pays you for taking no equity risk at all. So the bar is:

Required return = risk-free rate + equity risk premiumThe equity risk premium is the extra return you demand for standing at the back of the queue.

On 1 January 2026, Aswath Damodaran’s implied ERP for the US was 4.23% — which, given the market level, implied an expected return on US equities of 8.41%.

That is the bar. Roughly 8%.

A stock with a 3% free cash flow yield is not automatically a mistake — but it has to grow that cash flow fast enough to clear a hurdle around 8%, and “it will grow into it” is a claim, not a calculation. Make it a calculation.

The hurdle is not a constant, and this is where people get lazy

On 1 January 2026, the ten-year US Treasury was around 4.2%.

By mid-July 2026, it was around 4.6%.

Forty basis points, in six months. The hurdle went up — and nothing whatsoever changed at the companies.

A stock that was fairly priced in January is, on identical fundamentals, less attractive in July. Not because the business got worse. Because the alternative got better.

Look the number up on the day you are deciding. The Treasury publishes it daily, for free. Using a rate you memorised six months ago is not analysis; it is nostalgia.

Three filters before you ever click Buy

1. Does it earn more than its capital costs?

ROIC — return on invested capital. What the company earns on the money it puts to work.

The test: is ROIC consistently above the cost of that capital?

If yes, every euro reinvested creates value, and the business is a compounding machine.

If no, then growth actively destroys shareholder value. The company is burning capital to become larger, and larger is not better.

Which means the phrase “the company is growing fast” is, on its own, not a reason to buy anything. It might be the reason to run.

2. Is the free cash flow yield in the sane range?

See above. And know which side of the range you are on, and why.

3. What is management doing with the cash?

Because after the bills are paid, somebody decides where the residual goes — and it is not you.

- Empire building — overpriced acquisitions that make the CEO’s job bigger and your claim smaller

- Buybacks at high prices — destroying value with a shareholder-friendly label on it

- Buybacks when the stock is genuinely cheap — one of the most effective things a management team can do

- Dividends — simple, visible, and in many jurisdictions less tax-efficient than the alternative

And one question that gets skipped every time: does this position actually diversify you?

If your core is already heavily weighted to US technology, and your “conviction pick” is another US technology company, you have not diversified.

You have doubled down and called it a strategy.

A word about insider selling, because the internet gets this backwards

You will see a lot of content telling you that executives selling stock is a bearish signal.

It usually means nothing.

Most executive selling is scheduled months in advance under pre-arranged plans, or happens simply because a large share of that person’s pay is in stock and they would like to diversify, or buy a house, or pay a tax bill. Reading intent into it is a reliable way to be wrong.

The asymmetry runs the other way.

Insiders sell for a hundred reasons. They buy for one.

Cluster buying — several insiders purchasing on the open market, with their own money, at the same time — is the pattern worth your attention. It is rare, it is public, and it is the closest thing to a signal in this area.

The leak nobody fixes

Finally, the cost that has nothing to do with picking well.

If you hold US shares directly as a European investor, the United States withholds 30% of your dividends by default.

File a W-8BEN with your broker — certifying your residence and claiming your treaty rate — and that typically drops to 15%, which can often be credited against your domestic tax.

On a $1,000 dividend: $700 without the form, $850 with it.

Every year. For as long as you hold.

Your broker has the form. It takes minutes. And if you have never filed one, you are handing roughly half your dividend income to an administrative oversight — which is a genuinely stupid way to underperform.

And now the honest part

Should you be picking individual stocks at all?

Mostly, no. And the reason is not that you are not clever enough.

It is time.

Reading a 10-K properly, modelling free cash flow, tracking capital allocation, checking the hurdle rate — that is real work, and it repeats for every holding, forever. Below a meaningful portfolio size, the hours cost more than a point of outperformance is worth. And the evidence on professional stock pickers, who do this full-time with research teams, is not encouraging.

So the sane structure is a core and a satellite:

- The core — the large majority. Low-cost, broadly diversified index funds. It captures the growth of the market and does not depend on you being right about anything.

- The satellite — the small minority. Individual positions, where you have a genuine edge.

The point of the split is not diversification. It is that being wrong in the satellite is survivable, because the core never depended on you.

And “a genuine edge” almost always means one thing: you understand an industry because you work in it, better than an analyst in New York reading about it. That is a real advantage. Enthusiasm is not.

The three laws

One. Price the cash, not the earnings. FCF yield against the hurdle — and look the hurdle up today.

Two. Core for safety. Satellite for conviction. Never the other way round.

Three. Audit the leak. Tax forms and structure will cost you more, reliably, than any single stock pick will ever make you.

Treat shares like lottery tickets and the market will eventually audit your account.

Treat them as what they are — a legal claim on future cash, standing last in the queue — and you are finally playing the same game as the people on the other side of your trade.

Educational content only — not investment advice, and not a personal recommendation. No specific company is named here on purpose: a valuation true this quarter can be false the next, and a method ages better than a tip. Speak to a qualified, licensed professional before acting.

Primary sources

- 01Implied Equity Risk Premium, 1 January 2026: 4.23%, implying an expected return on US equities of 8.41% — Aswath Damodaran, NYU Stern

- 02Equity Risk Premiums: Determinants, Estimation and Implications — 2026 Edition — Aswath Damodaran / SSRN

- 03Daily Treasury Par Yield Curve Rates — the current risk-free rate, updated every business day — U.S. Department of the Treasury

- 04Form W-8BEN — Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding — Internal Revenue Service (IRS)

Questions people actually ask

What does it mean that a share is a 'residual claim'?

It means you are last in the queue. If the company goes bankrupt, the proceeds go first to the tax authority and secured creditors, then bondholders, then suppliers, then employees — and shareholders receive whatever is left, which is frequently nothing. That is not a technicality buried in a prospectus. It is the definition of equity, and it is the reason a share can go to zero while the company's bonds still pay out.

If shareholders get paid last, why would anyone buy shares?

Because of the asymmetry on the other side. A bondholder has priority, but their upside is capped: if the company invents something world-changing, the bondholder still receives their fixed coupon and not a cent more. A shareholder gives up priority and receives, in exchange, everything left over after the bills are paid — with no ceiling. You are trading safety for unlimited upside. That is a rational trade, provided you know you have made it.

Why is the P/E ratio unreliable?

Because the 'E' is an accounting construct rather than a fact. Earnings can be shaped by depreciation policy, by non-cash charges, by one-off adjustments and by the timing of when costs are recognised. None of that is necessarily fraudulent — it is what accounting is. But it means the denominator of the most popular ratio in retail investing is a number that management has meaningful discretion over. Cash is much harder to fake.

What is free cash flow yield?

Free cash flow divided by market capitalisation, expressed as a percentage. Free cash flow is what remains after the company has paid for the maintenance and investment required to keep running — the actual money that could be returned to you as dividends or used for buybacks. A €10bn company generating €500m of free cash flow has a 5% FCF yield. It is the closest thing equity analysis has to a hard number.

What FCF yield should I be looking for?

There is no single right answer, but there is a useful range and there are two warning zones. Below roughly 2% you are paying a very large premium for growth that has not happened yet — the entire thesis rests on the future. Above roughly 8% you should be suspicious rather than delighted: the market may be telling you the business is in structural decline and the cash flow will not persist. The comfortable middle, broadly 4–8%, is where a business is generating real cash and is not being priced as a miracle or a corpse.

What hurdle does a stock have to clear?

The risk-free rate plus the equity risk premium — the extra return you demand for standing at the back of the queue. Damodaran's implied equity risk premium for the US at the start of 2026 was 4.23%, which combined with the market level implied an expected return on equities of 8.41%. That is the bar. A stock with a 3% free cash flow yield is not automatically bad, but it must be growing that cash flow fast enough to clear a hurdle in the region of 8% — and 'it will grow into it' is a claim, not a calculation.

Is the hurdle rate a constant?

No, and this is where most people using this framework go wrong. The risk-free rate moves. On 1 January 2026 the ten-year US Treasury was around 4.2%. By mid-July 2026 it was around 4.6%. That is a 40 basis point rise in the hurdle in six months — which changes what a fair price is, without a single thing changing at the company. Look the number up, on the Treasury's own site, on the day you are actually making the decision.

What is ROIC, and why does it matter more than growth?

Return on invested capital: what the company earns on the money it deploys. The test is whether ROIC is consistently above the cost of that capital. If it is, every euro reinvested creates value and the business is a compounding machine. If it is not, then growth actively destroys shareholder value — the company is burning capital to get larger, and larger is not better. This is why 'the company is growing fast' is not, on its own, a reason to buy anything.

Does insider selling mean the stock is going down?

Usually it means nothing at all, and this is worth being precise about. Most executive selling happens under pre-scheduled plans set up months in advance, or simply because a large part of someone's pay is in stock and they would like to own a house. Reading a bearish signal into routine sales is a reliable way to be wrong. The asymmetry runs the other way: insiders sell for a hundred reasons and buy for one. Cluster buying — several insiders purchasing on the open market at the same time, with their own money — is the signal worth attention.

What is the W-8BEN form, and what does it cost me not to file it?

The IRS form that certifies you are not a US person and are entitled to the reduced withholding rate under your country's tax treaty. Without it, the United States withholds 30% of your dividends from US shares. With it, that typically drops to 15%, and the 15% can often be credited against your domestic tax. If you hold US shares directly and have never filed one, you are giving away roughly half your dividend income to a form. Your broker will have it. It takes minutes.

Should I be picking individual stocks at all?

Mostly, no — and the honest reason is time, not intelligence. Reading a 10-K properly, modelling free cash flow and tracking capital allocation is real work, repeated for every holding, forever. Below a meaningful portfolio size the hours cost more than a percentage point of outperformance is worth, and the evidence on professional stock pickers is not encouraging either. The sane structure is a passive core with a small satellite for genuine conviction — and a genuine conviction usually means you know something about an industry because you work in it.

What is a core-satellite portfolio?

A large majority — commonly around 80% — in low-cost, broadly diversified index funds, which capture the growth of the market and are, in the useful phrase, safe to fail. Then a minority — say 20% — for individual positions where you believe you have an edge. The point of the split is not diversification for its own sake. It is that the core does not depend on you being right, so being wrong in the satellite is survivable. Nothing here is a personal recommendation.